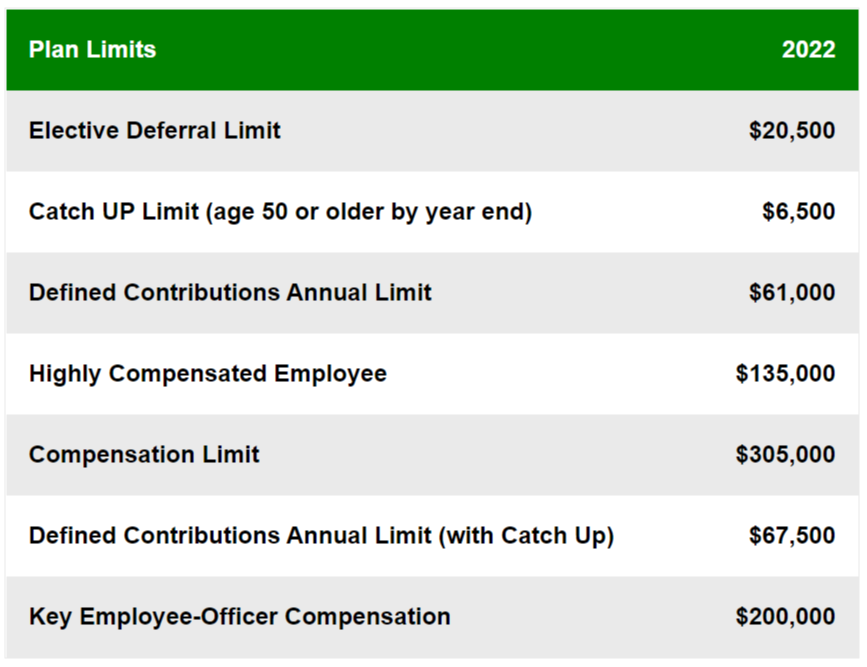

Many business owners and professionals use Cash Balance Plans to defer more than the maximum contribution of $61,000 into their 401(k). Candidates for Cash Balance Plans include business owners and professionals typically over age 45 who want to catch up on their retirement savings and earn more than $305,000 per year. The two main benefits of a cash balance are that contributions are tax-deductible to the business and builds retirement savings more quickly for plan participants due to the increased contribution limits.

A Cash Balance Plan is a defined benefit pension plan with a lifetime annuity that allows contributions that exceed the $61,000 limit. Cash Balance Plans can combine with a 401(k) plan. The employer funds 100% of the Cash Balance Plan and offers a 401(k) employer match to employees who contribute their required contribution to a 401(k).

Cash Balance Plan employer contributions for executive-level employees usually amount to roughly 6.9% of pay compared with the 4.7% contributions that are typical of 401(k) plans only. - 2018 National Cash Balance Research Report

How Cash Balance Plans differ from 401(k)s

First, Cash Balance Plans are defined benefit plans, and 401(k) s are defined contributions plans. Cash Balance Plans differ in these distinct ways:

Participation - Cash Balance Plans do not depend on employees contributing part of their compensation to the plan. However, a 401(k) plan depends on an employee contributing to the plan.

Lifetime Annuities - Unlike 401(k) plans, Cash Balance Plans are required to offer employees the ability to receive their benefits in the form of lifetime annuities.

Investment Risks - The investments of Cash Balance Plans are managed by the employer or an investment manager appointed by the employer. The employer bears the risks of the investments. Increases and decreases in the value of the plan's investments do not directly affect the benefit amounts promised to participants.

Federal Guarantee - Cash Balance Plans are defined benefit plans and are usually insured by the Pension Benefit Guaranty Corporation (PBGC), which is a federal agency.

Portability- In the event of a change in job or termination of the employee, distribution options include an annuity, lump-sum payout, or a rollover to an IRA.

If you're a business owner looking for strategy to potentially save more for retirement and pay less in business taxes, we can help! Greener Path Retirement Planning works with business owners and professionals to help them save money and accumulate retirement wealth with qualified retirement plan strategies, including Cash Balance Plans.

Contact our office to figure out which plan best suits your business >

Sources:

https://www.investopedia.com/terms/c/cashbalancepensionplan.asp

A Cash Balance plan may be appropriate for businesses with consistent revenues for long-term funding where owners are older and earn more than the average employee. These types of plans have additional costs and generally involve engagement of an actuarial firm for plan administration. This information is not intended as authoritative guidance or tax or legal advice. You should consult your attorney or tax advisor for guidance on your specific situation. In no way does advisor assure that, by using the information provided, plan sponsor will be in compliance with ERISA regulations.

LPL Tracking #1-05262207